Understanding IDC

Learn more about indirect costs for conducting research.

Indirect costs—sometimes referred to as Overhead or IDC or Burden (in OFC) or Facilities and Administrative Costs (F& A Costs)—are those costs not specifically identifiable for any one project or program, but which are valid expenses of conducting research, instruction, and other sponsored activities at UCSD. For example: building use, equipment depreciation, operation and maintenance of UCSD facilities, student services, departmental administration, or administrative support offices.

Indirect Cost Method

Indirect Cost Rates can be set at the task level. In situations where we have multiple rates under a single award, the burden schedule (IDC rate) can be set and overriden at the award, project, and task levels as needed.

Equipment and indirect costs

- Expenditures for items defined as inventorial equipment ($5,000 or more) are not included in the base used to calculate indirect costs (IDC) and therefore do not incur IDC.

- Equipment is identified as an item of non-expendable, tangible personal property, meaning it can be appraised for value, has an acquisition cost of $5,000 or more, is free-standing or can stand alone, and has a normal useful life expectancy of one year or more.

- As of July 1, 2006, expenditures for items defined as non-inventorial equipment ($1,500 – $4,999) are included in the IDC base and incur IDC.

Federal awards

For federal awards, the negotiated federal IDC rate, called Modified Total Direct Cost (MTDC), excludes the following expense categories:

- Equipment

- Capital expenditures

- Patient care

- Tuition remission

- Rental of off-site facilities

- Scholarships and fellowships

- Subcontracts in excess of $25k each

- Non-conference-type participants costs (536700 - Participant Costs)

- Cloud Computing Costs via UC San Diego Contracts with:

- Amazon Web Services

- Microsoft Azure

- SDSC Cloud

- Triton Shared Computing Cluster (TSCC)

- SDSC Project Storage

- Sherlock Cloud

Other awards

For all other awards,the IDC rate and exclusions vary. After receiving the award, Sponsored Projects Finance (SPF) reads the award document and sets up the IDC rate and exclusions in the accounting system. Always refer to your award documents for specific exclusions.

For more information, see the Contract and Grant manual.

IDC For Different Sponsor Types:

Federal awards

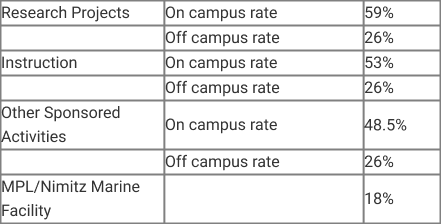

All proposal budgets that are submitted to funding agencies must provide for the recovery of indirect costs using the appropriate negotiated rate. For budgets that are being submitted to the Federal Government or For Profit agencies, there are five categories of federally negotiated Indirect Costs rates for

- UCSD:Research

- Instruction

- Other Sponsored Activities

- The Nimitz Marine Facility

- The General Clinical Research Center

Indirect Cost Rate Agreement dated June 6, 2024.

OMB Circular A-21 requires that indirect costs be allocated on the basis of modified total direct costs (MTDC).

UC programs

- For the following three programs, the IDC rate is 25% using the standard federal MTDC base:

- California Breast Cancer Research Program (CBCRP)

- California HIV/AIDS Research Program (CHRP)

- Tobacco-Related Disease Research Program (TRDRP)

- All other University of California (UC) programs do not have any indirect costs, so the rate is 0%. So, all costs are direct costs.

Non-profit and other non-federal agencies

- Non-federal funding agencies have their own unique indirect cost rate and base on which it's assessed.

- Not all funding agencies recognize the Federal MTDC base, e.g., some funding agencies may not consider equipment or tuition remission to be an exclusion from indirect costs.

- Please refer to the agency's guidelines to determine their policy and requirements on direct costs, indirect costs, and the appropriate exclusions to be calculated for your proposal budget

Industry programs

information on this policy, please see the Industry section.

MTDC Exclusion & How to Identify

Equipment and capital expenditures

The University defines equipment as an item of nonexpendable, tangible personal property which has an

acquisition cost of $5000 or more and has a normal life expectancy of more than one year.Costs for equipment leases or rental of equipment are included in the MTDC base unless the equipment lease includes an option to purchase. Equipment leases with option to purchase, since they are considered capital expenditures, are excluded from the MTDC base.

For fabricated equipment, all materials, supplies, and services from outside vendors or authorized internal

recharge activities used in the fabrication process are exempt from indirect costs if title is retained by the

University and the item has a life expectancy of more than one year.

Department labor, travel or other operating expenses associated with the fabrication such as salaries of Principal Investigators, graduate student researchers, or other comparable personnel who participate in the fabrication process are not included in the acquisition cost of the item and are subject to indirect costs. For more information on the treatment of fabricated equipment, see Accounting Manual Chapter P-415-32 and Contract and Grant Manual sections 2-526, 7-205, and 15-240.

Capital expenditures include building alterations or renovations or new building costs.

Patient care costs within research budgets

Patient care costs are defined as the costs of routine and ancillary medical services provided to individuals

participating in research programs by a hospital or clinic, including University and affiliated hospitals and clinics, but not laboratories of academic departments or organized research units.

Such costs are allowable charges to the research budget and are excluded from the MTDC base for purposes of determining indirect costs applicable to the project. Such costs differ from expenses for patient care that would have been incurred regardless of the research study; costs not affected by the research study are not allowable charges to the research budget.

Patient care costs should be based on a currently effective DHHS-negotiated patient care rate agreement or equivalent. However, when determining what items are excluded as patient care costs from the indirect cost base in a proposal budget, patient care costs do not include: consulting physician fees; personal expense reimbursement (such as human subject fees and patient travel) or any other direct payments to patients, including inpatients, outpatients, subjects, volunteers or donors; and costs of ancillary tests performed in facilities outside the hospital on a fee-for-service basis (e.g., in an independent, privately owned laboratory) or in an affiliated medical school/university based on an organizational fee schedule [NIH Grants Policy Statement].

Thus, these costs are not considered patient care costs for indirect cost purposes and are included in the MTDC base for the purpose of calculating the indirect costs applicable to the budget. A project which does not have an Institutional Review Board (IRB)- approved human subjects protocol may not incur patient care costs. For further details about the treatment of patient care costs in a proposal budget, see Chapter 7-211, Budget Patient Care.

Tuition remission

health insurance for University students.

Rental costs

Scholarships and fellowships

Subawards under grants, cooperative agreements, and contracts

When a contract, grant or cooperative agreement includes the transfer of a portion of the substantive work of a sponsored agreement to a third party, such work may be obtained by a contract, subgrant, subcooperative agreement, or subcontract.

These instruments used to obtain performance of substantive work by third party entities are all referred to as subawards. Uniform Guidance or 2 CFR 200 permits the application of the indirect cost rate to the first $25,000 of each subaward by including this amount in the MTDC base.The portion of each subaward in excess of $25,000 is excluded from the MTDC base. This limit applies to the duration of the subaward.

However, when campuses have the option to issue a new subaward pursuant to a renewal, extension or

supplemental award from the prime sponsor based on a competing proposal subsequent to the initial award and that renewal provides for additional work and increased funding for the subawardee, indirect costs are assessed on the first $25,000 of the new subaward.

Purchases of standard commercial goods or services such as routine testing, administrative support, or

consultant agreements are not considered subawards for this purpose, are not included in the subcontract line item of a proposal budget, and are not subject to the $25,000 limit for application of overhead.