Student Travel

Last Updated: January 10, 2025 2:05:56 PM PST

Give feedback

Learn the different types of travel for students. Find out how to book and pay for business travel for students.

We value the chance for enrolled students to engage in travel as a component of their academic and extracurricular activities. Given UC San Diego's evolving status as a globally-focused institution in teaching, research, and service, such travel experiences frequently encompass both international and domestic destinations.

In general, UC San Diego payments for student travel will take one of two forms:

UC San Diego business-related (nontax reportable) OR scholarship/fellowship (tax reportable).

Learn about the important distinction between official student business travel and providing financial support. The explanations below are not all-inclusive and determinations may need to be made on a case-by-case basis.

UC San Diego business-related student travel.

Student travel is generally considered UC San Diego business-related travel (nontaxable, nonreportable) if:

Examples of UC San Diego business-related travel include:

- Student travels to represent UC San Diego in a scholastic or athletic competition.

- Student travels to present at a conference, where the student's name (and that of UC San Diego) is published (poster, website, brochure, program) as a presenter at the conference.

- Student travels to perform research for her dissertation. This would qualify if UC San Diego would otherwise perform research on this topic, regardless of the student's research – as such, UC San Diego is considered the primary beneficiary.

- Student travels to conduct dissertation research and has obtained his or her own external funding (including external fellowships) to support their research, with the funding provided to the University to administer either under a faculty PI or with the student serving as PI.

To document such business-related travel by a student, UC San Diego uses the UC San Diego Student Certification for Business-Related Travel form and supporting documents. The form must be completed and attached to the Concur Travel Request as a pre-authorization. Please download the form to view the required fillable fields. (See “Step-by-Step Process for Requesting Payments” below.)

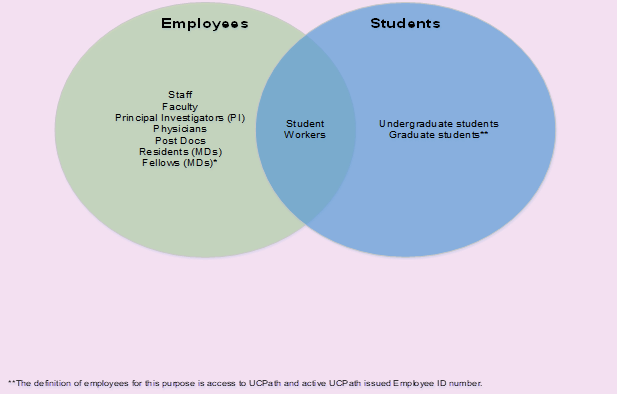

Note: If it is determined the student will be on UCSD Business-related travel, the next step is to determine if the student is an employee or non-employee and follow the appropriate steps listed in the “Step-by-Step Process for Requesting Payments” section.

Paying for student business travel expenses.

When a student travels for UC San Diego business, it is generally expected that all or most of the travel will be paid by UC San Diego as opposed to the student paying out-of-pocket for the majority of the expenses.

- The UCSD CTS card is saved in Concur/Balboa for departments to use to pay for student airfare.

- For situations where the University isn't able to pay for the Student's travel expenses (e.g. Meals & Incidentals, Hotel, Registration, Rideshare), the Travel & Entertainment - Temporary Virtual Card (T&E-TVC)is a great resource to utilize!

Scholarship/fellowship payment toward student travel.

When student travel does not meet one of the above criteria, a payment is considered a non-qualified scholarship/ fellowship. A scholarship/fellowship is a payment or reimbursement to a student to aid their study, training or research. It includes payment towards tuition, fees, living expenses and travel expenses.

Use for qualified expenses is nonreportable and nontaxable. Use for nonqualified expenses is reportable and may be taxable.

The student travel payment is generally considered to be scholarship/fellowship (taxable, self-reportable by the student) if:

- Reimbursement is made for activities in which UC San Diego is relatively disinterested or the research is student-led.

- The project/research's primary purpose and original intent is to further the student's education or training.

- UC San Diego obtains little or no benefit.

- Activities are performed to contribute to the development of the skills needed in the student's studies.

Examples of Scholarship/fellowship for Nonqualified Expenses:

- Student travels for dissertation research that is not research UC San Diego would otherwise conduct – the student’s dissertation is the primary purpose of the travel and the student is the primary beneficiary.

- Student travels for sign language training, which will assist in communication needed for the degree. This is supplemental work that the student may need to succeed, but it is not a required part of the degree.

- Student receives a department award to be used towards pursuing academic activities (such as travel to attend a conference). The award may be provided to all students within a degree program or granted based upon an application/essay award process.

NOTE: Payments for ‘services performed’ is considered compensation and must be paid through payroll, and foreign students must meet all visa requirements.

Taxes and reporting for UC San Diego student travel.

U.S. citizens and resident aliens

- Business-related travel is nonreportable and nontaxable.

- Qualified scholarship/fellowships are nonreportable and nontaxable.

- There is no tax withholding requirement for nonqualified scholarship/fellowship payments, but this income is reportable by the recipient. This income is not reported on a tax document (e.g., W-2 or 1099) but is considered to be self-reported income per IRS publication 970.Students may be required to pay estimated quarterly taxes to federal (IRS form 1040-ES) and state revenue offices on this income. Students should consult a tax professional on how to treat these payments for tax purposes.

- For a U.S citizen or resident alien (undergraduate or graduate students), payment is considered as taxable nonqualified scholarship/fellowship income and is reported by UC San Diego to the IRS. It is the student's responsibility to maintain records for these payments (students should consult a tax professional on how to treat these payments for tax purposes).

Foreign students (nonresidents for tax purposes)

- Business-related travel is not considered reportable or taxable income.

- In general, the taxable portion of a scholarship/fellowship paid to a foreign student is subject to federal income tax withholding at the rate of 30%, unless the payments are exempt from tax under the Internal Revenue Code or a tax treaty. However, payees who are temporarily present in the United States in F-1, J-1, M-1, Q-1, or Q-2 nonimmigrant visa status are subject to a reduced 14% withholding rate on the taxable portion of the grant because such individuals are considered to be engaged in a U.S. trade or business under Internal Revenue Code section 871(c). This income is reported on tax document 1042S. Students may be required to pay estimated quarterly taxes to federal (IRS form 1040-ES) and state revenue offices on this income. Students must hold the proper visa to receive such scholarship/fellowship payment.

- A GLACIER record must be completed.

- Payments to nonresident aliens will be reported on form 1042S and may be subject to tax withholdings.

- Before a foreign student travels, make sure they have the proper visas to receive reportable compensation if the travel is determined to be a scholarship/ fellowship for nonqualified expenses. Students are subject to visa requirements of their destination as well as any restrictions set by their student visa if an international student

Step-by-step process for requesting payment.

- Business-related travel reimbursement process

- Complete the Student Certification for Business-Related Travel and supporting documents. The form must certify that the student travel qualifies as UC San Diego business-related, and be signed by the student and the faculty member or Principal Investigator (if paid from a federal grant).

- Review University Travel Process for guidance on what to do before, during , and after travel including important guideline such as meal and lodging caps, mileage reimbursement rates, conference registration or hotel deposit, requesting a wire and much more.

- Review and consider applying for UCSD available payment products.

- If student employee, Create a new Travel Request in Concur, and Travel Expense Report. Include the completed Student Certification for Business-Related Travel and supporting documents.

- If student non-employee, register in PaymentWorks. Create a new Travel Request in Concur, and Travel Expense Report for Non-Employee (Guest)

- Scholarship/fellowship payment for travel as a nonqualified expense

- For UC San Diego students, scholarship/fellowship payments should be processed through the Financial Aid Office/Graduate Division.

- If the recipient is not a UC San Diego student, then the payment should be entered online using the Payment Request form and must include supporting documents.

Financial Aid & Additional resources.

- Graduate student financial support: submit a ticket at https://support.ucsd.edu/students

- type "Graduate Student Fellowship Stipends" in the *More Specificallyfield; the other fields will then auto-populate

- Undergraduate scholarships: complete an Undergraduate Scholarship Payment Request Submit questions to scholarships@ucsd.edu

- Health sciences financial support: somfinaid@health.ucsd.edu, (858) 534-4664

IRS Scholarships, Fellowships, Grants, and Tuition Reductions

IRS Topic 421 – Scholarship and Fellowship Grants

IRS Withholding Federal Income Tax on Scholarships, Fellowships, and Grants Paid to Aliens

Find answers, request services, or get help from our team at the UC San Diego Services & Support portal.