SSA Guidance

The SSA guidance and practices is located on this page.

Overview

A Sales and Service Activity (SSA) is an activity that provided specific, ongoing, repetitive goods or services to campus units on a fee basis. Sales and services provided to an external entity are not achieved by the internal recharge mechanism. Rather charges and revenue are processed by a billing invoice and a cash receipt or credit card transaction.

For guidance related to other type of activity that uses the recharge mechanism, please follow the link below;

If you or your department is interested in establishing a Recharge and are unsure what activity best describes the operation, please do not hesitate to contact Recharge@ucsd.edu to discuss options.

The basic guidelines that must be adhered to at UCSD when establishing and managing a SSA are;

- SSAs are to operate on a The costs to operate a SSA may not include a profit on any rates charged to internal customers.

- Costs used to develop rates must be allowable, allocable, reasonable, necessary, and consistently treated.

- Salaries and wages should reflect the percentage of effort dedicated to the operation and services/products provided.

- Rates cannot discriminate between customers. The unit cost must be consistently applied to all users, irrespective of funding source, and charges must be allocated to users based on actual use.

- Capital equipment cannot post to SSA operating funds. Instead, the depreciation for that equipment must be factored into the rate calculation.

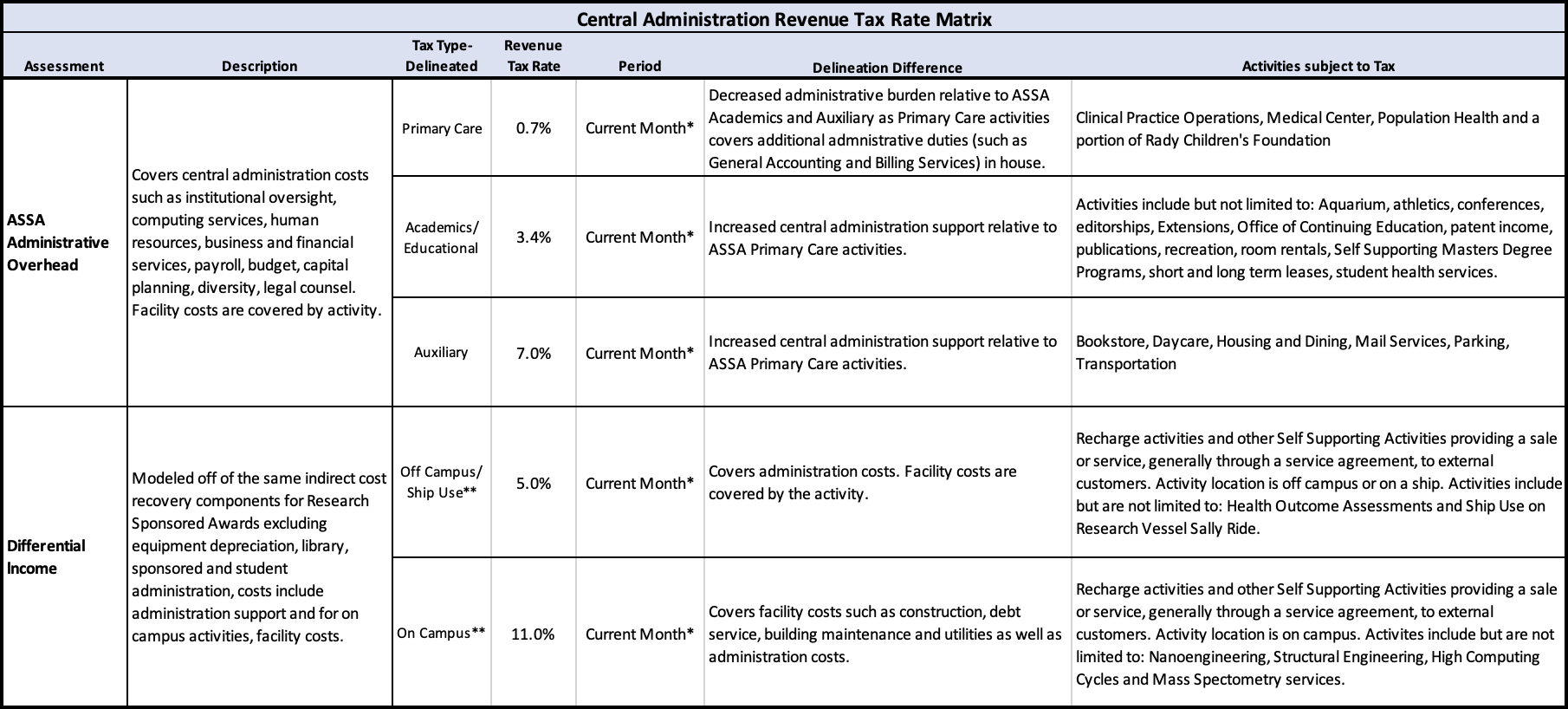

- A minimum of 11% assessed on revenues for overhead cost recovery (Differential Income) must be included in all rates charged to external customers for on-campus activities.

- Services or products sold to the general public must remit any necessary California sales and/or other unrelated business income tax.

- Subsidies cannot discriminate between users and must be disclosed in the rate proposal, including amount, purpose, and funding source.

- Originating Departments or units are to document and maintain records of expenditures, billings, and cost transfers.

Deviations from these guidelines may be necessary under special circumstances. Any deviation should be reviewed and approved by the BFS - Financial Analysis Office (FAO).

Breakeven

Based on UCOP policy, a SSA will be operated on a breakeven or no-gain/no-loss basis. This means rates are to be developed with the intention of recovering only allowable costs. No profit or markup is to be added to any rate recharged to federal customers.

Any surplus or deficit occurring in any one year will be corrected by adjustment of rates in the succeeding year to achieve a breakeven balance at the succeeding year end. Every effort should be made to ensure that year-end surpluses or deficits do not exceed two months (16.66%) of the SSA’s annual expenses.

The adjustment of rates will generally be based on estimates since actual performance data for the year will not be available prior to the development and publication of the succeeding year's Recharge rates. In exceptional cases when such an adjustment would create a severe fluctuation in rates from one year to the next, achievement of a breakeven balance can be extended for a reasonable period beyond the succeeding year upon approval by the BFS - FAO. Accordingly, the BFS - FAO may also approve the maintenance of surpluses in excess of two months of the SSA's annual expenditures when appropriate.

Cost Treatment

Costs included in Recharge rate development must meet all cost principles per university and governmental policies and guidance.

For more details on cost treatment, click here.

Overhead Cost Recovery (Differential Income)

Campus assesses SSA the central administration's portion of differential income. SSAs are allowed to accumulate funds in the OFC Differential Income Fund.

Each Vice Chancellor area may also require a minimum Differential Income portion to be remitted to the Vice Chancellor responsible for the activity. Consult your Vice Chancellor’s office for more information.

For more details on differential income, click here.